Market analysis of conifer pulpwood – how to get the best prices

Tracking prices on national and regional level is, however, not enough to maximise the timber sales income for our clients. Timber prices are very dynamic in terms of both time and geography and therefore always determined by a combination of geography, location of off-taking industries and general market conditions.

To illustrate the importance of timing and geography HD Forest made an analysis of conifer pulpwood price variations based on the properties we manage in Estonia. We used pulpwood roadside prices for August 2019 as well as delivered prices to harbours, bigger pellet factories and firewood market prices for January and August.

The analysis resulted in the following three maps:

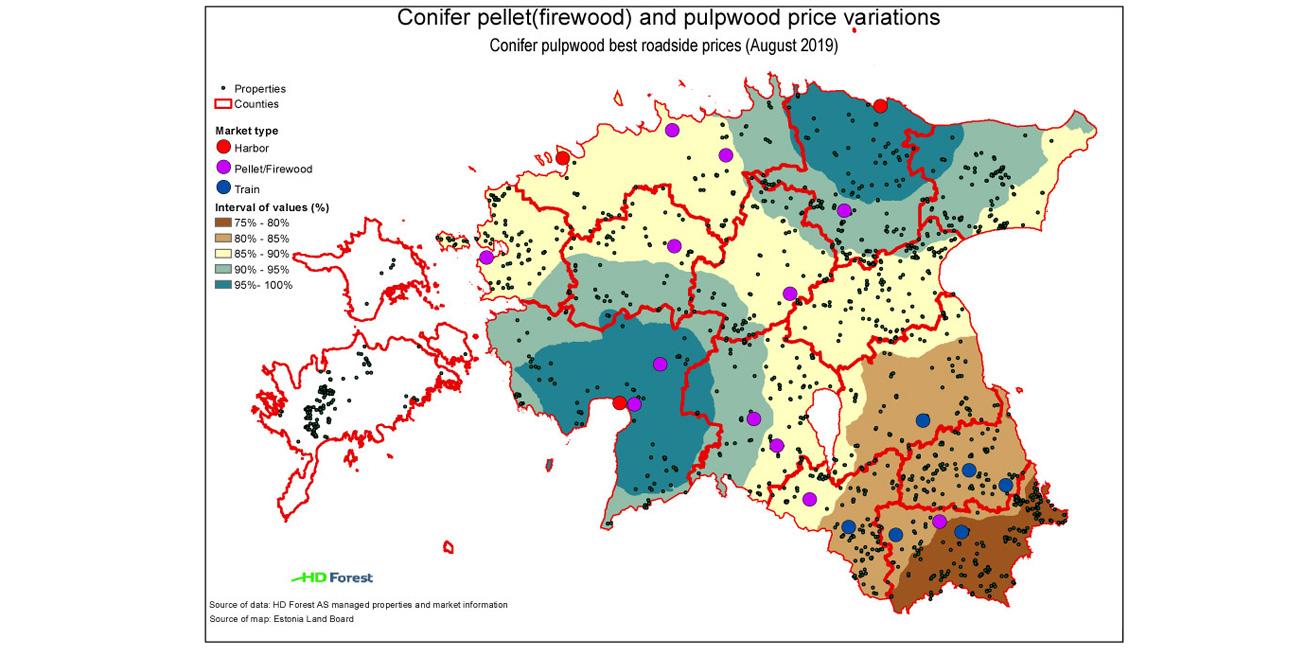

1. “Conifer pulpwood best roadside prices (August 2019)”. Best roadside price for conifer pulpwood in August 2019. This map is showing the maximum conifer pulpwood roadside prices in different parts of the country. The best pulpwood prices at that time were achieved in the harbours (Kunda and Pärnu). Prices in the south-east of Estonia are lower, because this area is far from the harbours and transport costs are therefore higher.

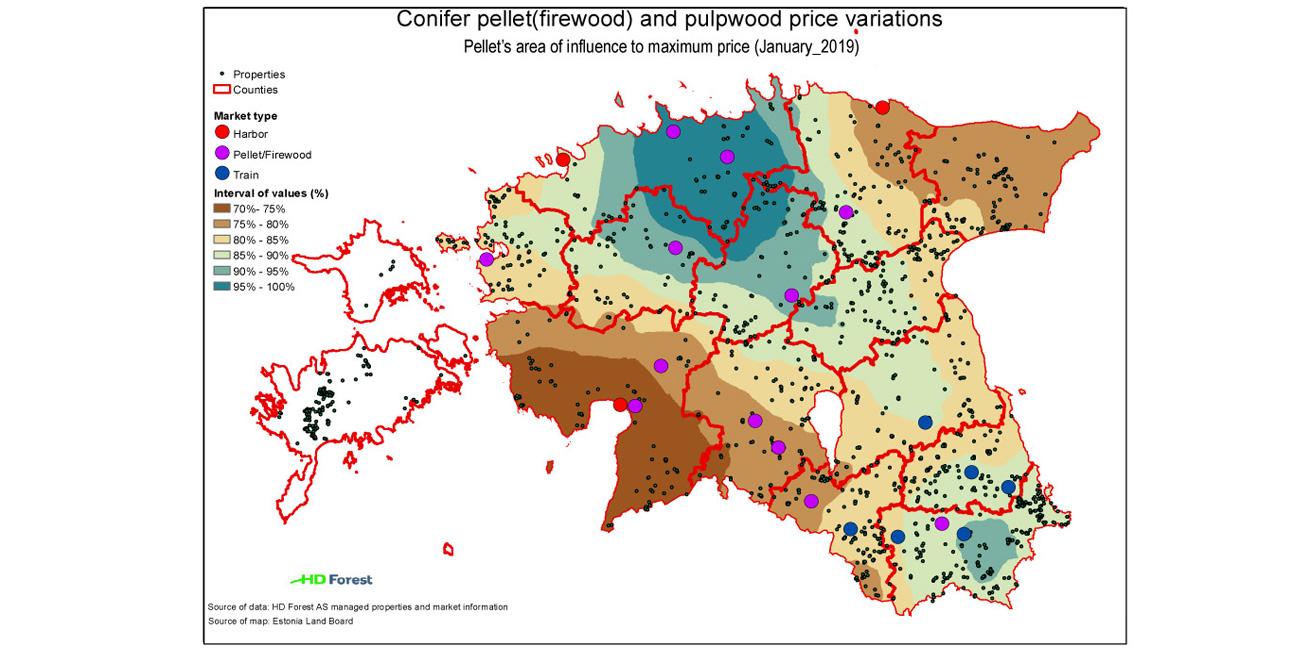

2. “Pellet’s area of influence to maximum price (January 2019)”, is basically showing the areas where pellet factories have the power to compete with the harbours. Here were compared best pellet price vs best roadside pulpwood price. Puplwood prices were very good in January and for pellet factories it was hard to compete with the harbours. In January, biggest influence had Kehra pellet buyers (in the north) and Osula pellet buyers (in south-east). So, on those areas it would have been more reasonable to sell the material to those pellet factories, not to harbours.

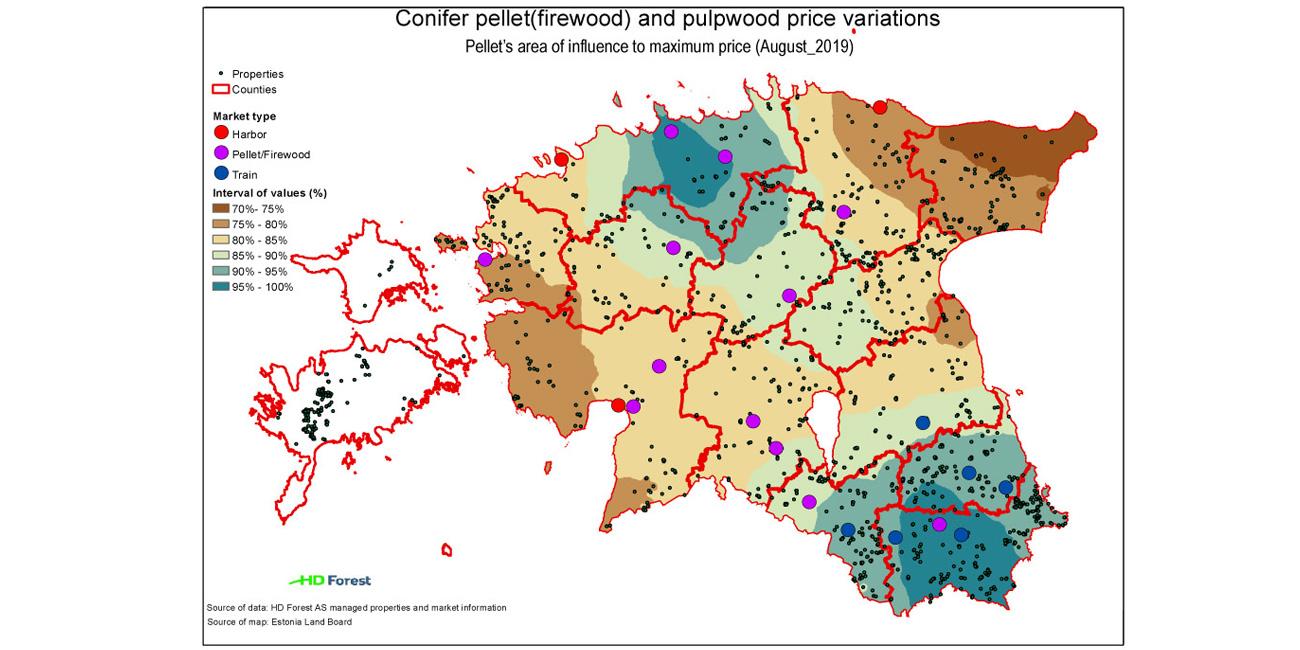

3. Third map “Pellet’s area of influence to maximum price (August 2019)”, is showing the same as the previous map, just used were August 2019 prices. It shows that south-east corner has more power to compete with harbours and has increased its influence area. Since January 2019, pulpwood price had decreased by around 20 EUR. Consequently, pellet producers have more options/possibilities to compete. Also, railway has its impact, now it’s more felt (south-east of Estonia).

Continuous monitoring and analyses of these localised price trends enable us to maximise the timber sales for our customers as part of the management service provided by HD Forest.